Market Update: Poor Switzerland, poor statisticians, oblivious investors

After last Friday afternoon’s wobble, markets regained their footing. Global stocks mostly recovered and are back within touching distance of all-time highs. Investor sentiment was aided by the slew of US trade deals – either signed or pending.

Amongst the ‘deal’ exceptions was Switzerland, after being hit with an unexpected 39% US tariff. The Swiss President flew to the US but failed to get a meeting with Trump, or any concessions from foreign secretary Marco Rubio. This is despite the majority of the Swiss trade surplus deriving from US demand for small lots of physical refined gold – essentially money – hardly something the Trump administration wants to shift production of to the US. Perhaps they are being singled out to encourage others to make deals.

Meanwhile, Trump fired the respected leader of the Bureau of Labour Statistics for releasing economic data he does not like, and then hired a friend to help set interest rates he does like.

One commentator described it as a descent into ‘Banana Republic’ policy. So, it may seem odd that many investors feel that the most severe economic risks have diminished, allowing markets to push higher. To be clear, this is not the same as investors thinking everything is alright. The risks have shifted from fast-moving near-term policy uncertainty to a longer-term likelihood that policies will not benefit growth. Markets feel more pragmatic than optimistic, so it might be hard to find further gains over the medium-term.

The Bank of England’s hawkish cut

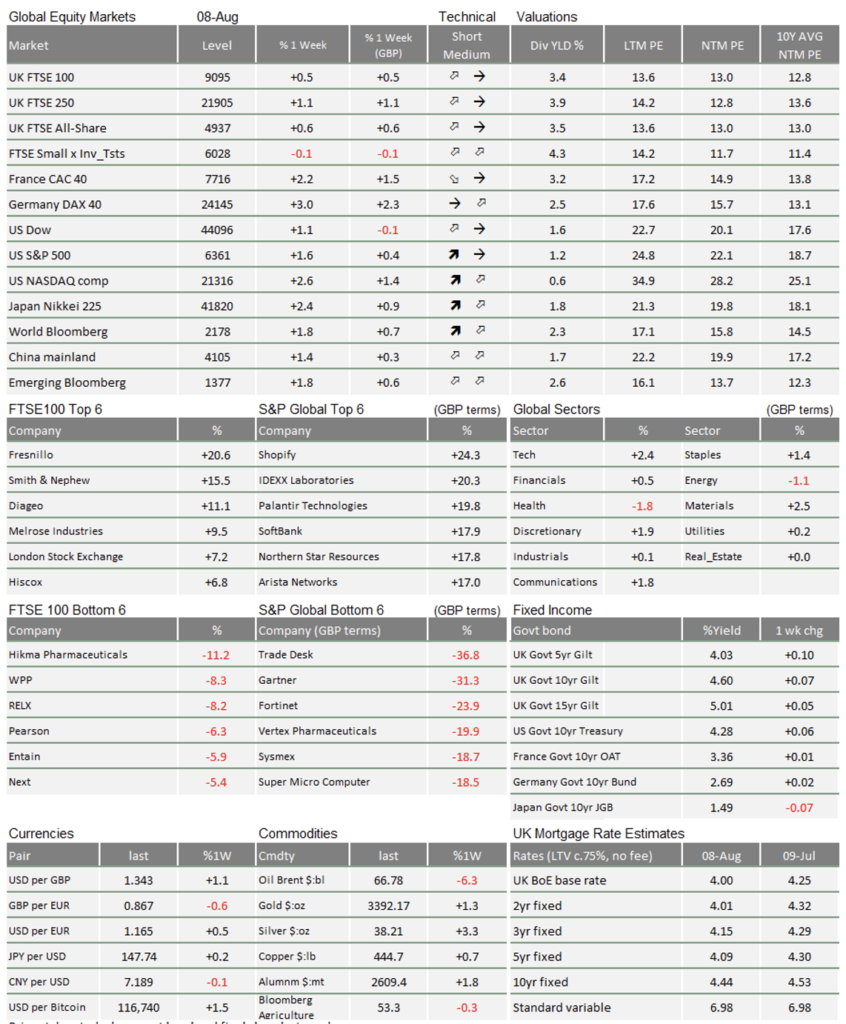

On Thursday the Bank of England (BoE) cut interest rates, as expected, for the 8th time since June 2024. What was not expected was the Monetary Policy Committee’s (MPC) razor thin 5-4 vote margin, with four members opting to hold rates steady. In fact, the MPC was initially deadlocked (one member voted for a larger rate cut) and required an unprecedented second vote to get rates lower. The hawkish dissenters were swayed by the BoE’s own forecasts showing higher inflation into the end of the year than previously expected. In response, bond markets dialled back their bets on further rate cuts.

Governor Andrew Bailey was one of those backing a cut. Interestingly, the governor also indicated that he supports the government’s desire to stimulate UK growth into the end of the year. In a sense, this shows Britain’s difficult position: despite sticky inflation, key indicators (like housebuilding and business construction) point to a weak economy.

The BoE’s hawkish turn on short-term rates did little to move long-term bond yields, partly because there was a hint that the central bank will slow its sale (think ‘re-privatisation’) of longer-dated UK government bonds from the “quantitative easing” stockpile it built up during the pandemic.

Before the BoE’s decision, there were multiple stories released about a multibillion “black hole” in the government’s finances. The presence of these stories – and the government’s lack of response or denial of them – suggests Downing Street is preparing to break one of its fiscal promises (backed up by reports in the Guardian). That might mean higher taxes, tweaking its ‘iron clad’ fiscal rules, or both. We devote a separate article this week to the risks and potential rewards of such a change.

Russia negotiations are a positive for Europe

The BoE’s hawkish shift pushed sterling up against the dollar – but less so against the euro, which itself strengthened. That strength was largely down to the week’s big geopolitical story: the US and Russia edging closer to ceasefire negotiations for Ukraine. Russia’s war on Ukraine, and the associated spike in European energy prices, has been the continent’s biggest headwind for years.

The Trump administration is taking a carrot-and-stick approach, pressuring Russia through secondary tariffs on India (for still buying significant amounts of Russian oil) while simultaneously angling for a Trump-Putin sit-down. As far as getting a meeting is concerned, the tactic seems to be working. And judging by markets’ reaction, investors expect ceasefire progress too.

Oil prices may have reflected this, as they came sharply down from last week. This was partly due to OPEC+ agreeing to loosen output constraints in September, but the India tariff suggests that Trump is serious about resolving the conflict, which would boost global oil supplies further.

The move down in oil was seen as a positive for most equities (with the exception of the aforementioned UK) but particularly Europe.

Tail risks fade, building momentum

Talk of a ceasefire helped investors’ sense that the tail risks – the worst-case scenarios that blight the market outlook – are receding. The same is true for tariffs, which have, for the most part, been further delayed or avoided through trade deals (with the exception again of poor Switzerland). Markets are feeling relieved; it could have been worse. That relief creates momentum in asset prices, as those betting against the market have to close their positions.

This momentum has been pushing up markets for several weeks, backed up by strong liquidity and a surge of buying from retail investors. It has tailed off a little, and equities are no longer bursting through all-time highs, but sentiment is clearly still strong. Strong earnings reports from the ‘Magnificent Seven’ US tech companies (retail investors’ darlings) have helped too.

Tail risks fading is not the same as everything being alright. While trade deals are being signed, average effective US tariff rates have risen close to 20% – their highest level in over 90 years. We still do not know how this will affect inflation and demand either in the US economy or elsewhere in the world.

Outside of the big tech companies, we can see the slowdown in US growth coming through in Q2 corporate earnings. The most recent data suggests the April-June soft patch is improving, but if high effective tariffs compress US demand further, markets will struggle to break higher from here. Encouragingly, markets feel that the US economy is resilient enough to muddle through some rough months with tariffs at their current levels – and so the world carries on.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.